20 years helping business leaders deliver alpha. View our success stories

20 years helping business leaders deliver alpha. View our success stories

Continuation Funds Surge

Continuation fund transactions surged to $63 billion in 2024, driven by a liquidity drought that left 29,000 unsold portfolio companies globally, valued at $3.6 trillion. Continuation funds have evolved from tactical fixes into strategic tools for investors seeking alternative liquidity solutions; marketed as holders of “trophy assets” rather than[1]“zombie funds”.

They allow GPs to retain high-performing assets while offering LPs the choice to cash out or roll over. This dual-track structure preserves upside potential, maintains investor alignment, and provides options — especially valuable in a market constrained by aging dry powder and pressure to return capital. However, the rise of continuation vehicles has raised concerns. When GPs sit on both sides of the transaction, conflicts of interest around fees, carry resets, and valuations can emerge. Leading firms are addressing these risks through independent advisory committees, third-party valuations, and transparent pricing mechanisms.

However, extended holding periods create an entirely new set of challenges for leadership alignment and commitment.

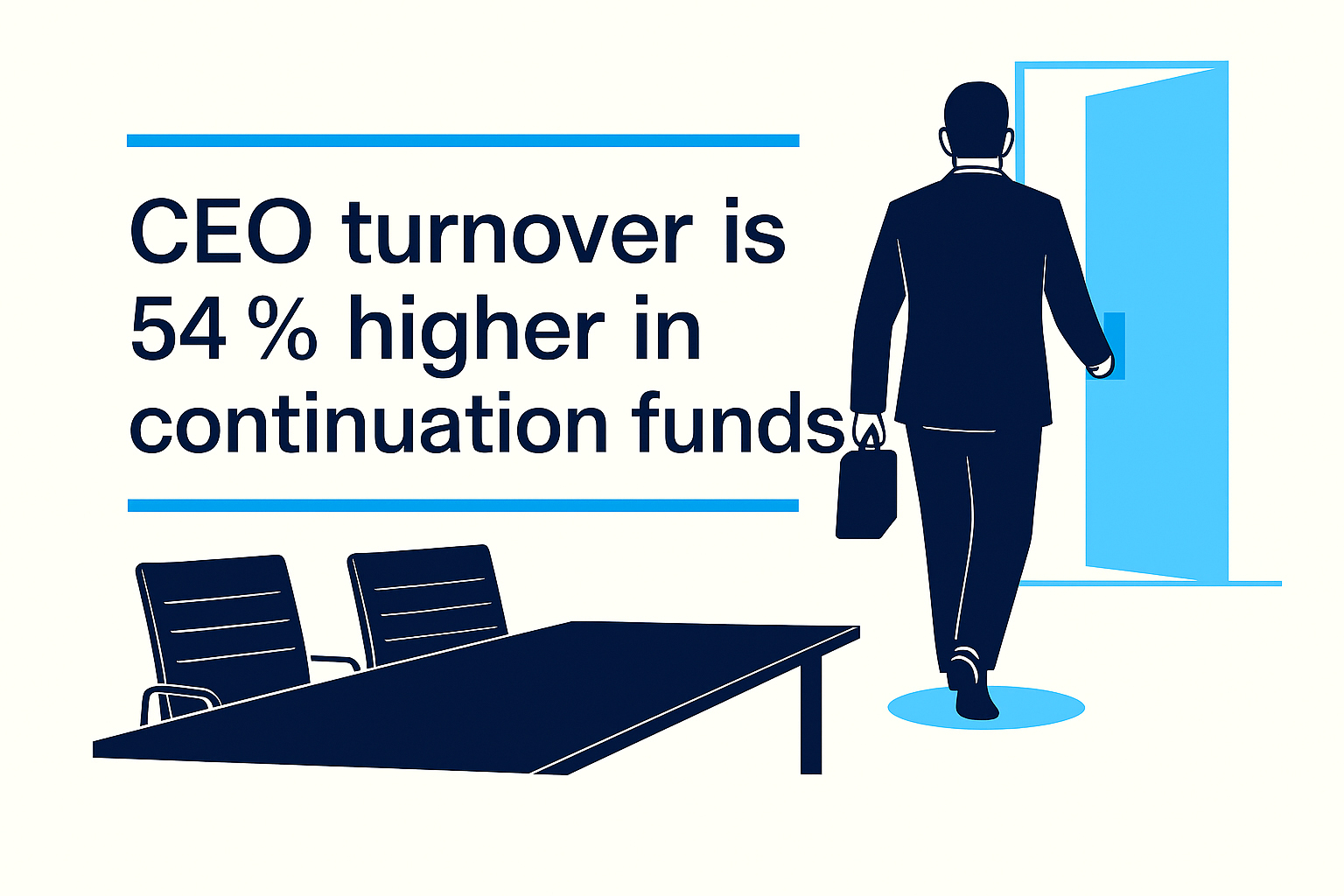

50%+ higher CEO turnover in continuation funds

CEO turnover has long been a major issue in PE-owned companies. Humatica’s research into unplanned CEO turnover across PE-backed companies reveals a consistent pattern: the primary cause of turnover is execution failure, not strategy. This risk is amplified in continuation fund contexts, where extended ownership demands renewed commitment and a reset of value creation drivers.

In continuation funds, leadership transitions are more frequent. In selected European funds, CEO turnover in continuation fund portfolio companies was 54% higher over the past five years. More than 65% of CEOs were replaced during the holding period. This reflects broader leadership restructuring as firms recalibrate for extended value creation.

Interviews with 20 European fund managers highlighted a recurring issue: insufficient focus on how growth plans will be executed. CEO turnover often stems from misaligned expectations and delayed interventions—leading to longer holding periods and lower IRR.

“We assume management teams can run with the plan

—experience shows this is rarely the case.”

“Issues which deal with people take time;

if you identify them early they can be resolved in time.”

“It’s in everyone’s interest to ensure support is provided for management

as early as possible to deliver the plan.”

Four Levers to De-Risk Execution and Boost Performance

To reduce CEO turnover and to ensure commitment to delivery of extended Value Creation Plans (VCPs), our survey identified four critical levers that private equity firms must address to successfully master extended ownership cycles:

1. Joint Renewal of the Value Creation Plan – Success depends not just on agreeing the growth ambition, but on jointly developing a realistic implementation roadmap with the management team. Collaborative preparation, expectation re-setting, and active implementation planning are essential. This ensures the team owns the extended plan and is equipped to deliver it.

2. Address emerging Management Capability Gaps – The capabilities required to execute the renewed plan must be openly assessed. Identifying gaps in leadership roles and functional expertise allows firms to intervene before performance suffers.

3. Embedded High-Performance Ways of Working – Organizational behaviours and collaboration are decisive for execution. Embedding high-performance norms and accountability helps align teams and sustain momentum across longer cycles.

4. Fixing bottlenecks in Management Processes – Execution often fails due to weak internal processes—especially in decision-making, reporting, and accountability. These must be identified and strengthened to support the next phase of growth.

These levers are especially relevant in continuation fund contexts, where sustained leadership and organizational resilience are essential. Leadership change may be necessary to unlock growth—but it is rarely a quick fix – and almost always comes at a cost to IRR.

Contact us to learn more about how you can boost performance during longer holding periods with Organizational Excellence.

Every significant technological shift in economic history has ultimately changed the shape of organisations — not just the tools they use, but their structures, hierarchies,…

Read more

This is the final article in a three-part series on designing and implementing a fit-for-purpose Target Operating Model. In Part I, we explored how to…

Read more

For the past three years, the AI conversation in business has been primarily about AI as an assistant — a tool that helps humans work…

Read more

Erhalten Sie jeden Monat Neuigkeiten und wertvolle Perspektiven zu Themen der organisatorischen Effektivität